Heaven’s Got A Plan For You: The MLS – Future of Organized Real Estate, Part 2

By

Rob Hahn

[I had planned on writing this much, much earlier… but as you might guess, a few things happened since Part 1 was published. Like a social media storm around the issue of bad behavior in the industry. Even as I hope for some positive changes, life goes on, and the industry itself does need fixing. So here we go with Part 2, which deals with the MLS.]

In Part 1 of this series, I laid out the outline of what must be done to lay the foundations for the next 100 years of organized real estate. A key insight was that the MLS and the Association are stuck in a dysfunctional co-dependent relationship that prevents both of them from being who each needs to be. The solution was divorce, which means a financial and organizational restructuring, to support the core mission of both the MLS and the Association. I had mentioned that I would go into more detail in a future post. Well, that post is this one.

It’s enormously long, but worth reading if you’re involved in the MLS in some way. For the TL;DR crowd, a summary:

Too many, too small, too poor — the MLS in a nutshell

Governance is broken

Divorce improves both the Association and the MLS

Restructure the MLS and privatize it

Restructure governance to provide both streamlined decision making and representation

Rethink the relationship between the Participant brokers and the MLS

Those who have heard me speak at CMLS 2016 in Las Vegas know the theme, but even they might benefit from a written explanation. So, let’s get into it.

Too Many, Too Small, Too Poor

It is simply beyond debate that there are too many MLSs in the United States. Last number I’ve heard from MLS people is that after ten years of consolidation, we are down to somewhere around 750 MLSs from 850 or so. At that rate, by year 2050, we’ll be down to 450 or so.

One of the primary motivations behind efforts like Project Upstream is the “overlapping market disorder” as Upstream’s primary consultant, WAVGroup put it in a blogpost last year:

Overlapping market disorder has plagued real estate forever. It has caused firms to enter and maintain data in multiple MLSs. Firms are also operating a wide range of back office data management systems, including franchise data management solutions. Replicating data is the process of storing the same information in multiple databases. It’s expensive and wasteful. Different data base formats also create incremental costs whenever systems need to share data. It requires data mapping and aggregation. Again, it’s expensive and wasteful.

That simply cannot be debated, and no one really does.

What isn’t thought of very often, however, is that the MLSs are simply too small and too poor to be competitive in the 21st century. I can’t find the stat right now, but it is said that the top 20 MLSs in the U.S. cover over 70% of the listings in them. The other 730 have the other 30%. There are hundreds of MLSs in the U.S. today with fewer members than the local country club.

There are a few reasons for the small MLS. Many are rural, and located hundreds of miles away from the nearest big city where the larger MLS is located. In other cases, it’s pure protectionism: the local brokers want to keep out competitors from the neighboring areas, so set up a MLS that they control with rules and policies designed to make it difficult for new entrants. Vacation markets or high-end luxury markets near major urban areas are a perfect example of this. And finally, the MLS and the local Association are joined at the hip, and the local Association doesn’t want to give up the cash cow that is the small MLS.

The consequence of the MLS being too small is that they are also too poor. This is the one that has people scratching their heads, because quite a few people are used to thinking of the MLS as this important institution with millions of dollars that sets the rules for how business can be conducted in a given area. The large MLSs, like CRMLS and MRIS, own buildings, have staff in the hundreds, and tens of millions of dollars in revenues and reserves. How the heck are they too poor?

Well, Gartner Research defines small businesses as organizations with less than $50 million in annual revenues. By that measure, there may not be a single MLS in the country that isn’t a small business. CRMLS, the largest MLS in the country, with over 82,000 members charges about $400 per year. Here’s a chart of what it costs to get CRMLS through OCAR, one of its larger Associations:

Well, $400 x 82,000 = $32.8 million, well short of the $50 million figure to be a mid-sized business. That’s the largest MLS in the country, which implies that everyone else is likely making less money.

Why the MLS is Poor and the Consequences of Poverty

There is a very simple, very good reason why the MLS is poor: it isn’t allowed to raise prices.

The MLS isn’t allowed to raise prices because it is owned and governed by the very customers to whom it sells its products and services. Nobody likes to pay more than they have to for a product or service, especially for a product/service that is mandatory to have, which takes on a local monopoly characteristic (thanks to the linkage to the Association), and feels more like a tax than a voluntary purchase.

I’m actually 35, but did a couple of MLS conversions…

Experienced MLS CEO’s and MLS Board members know that there are two things that would cause a firestorm of controversy within the MLS. First is changing the platform from one vendor to another; that process has given more than a few MLS CEO’s grey hairs.

The other is any talk of raising the price of the MLS. Oh, the hell that the Board and the membership would put the poor MLS CEO through for suggesting perhaps a $5 increase (less than two Starbucks regular coffees a month) to the price of the MLS!

More than a few MLSs in the U.S. today boast about the fact that they haven’t raised prices in years and years. “We haven’t raised dues in ten years!” is a common boast. But, despite historically low inflation rates (official inflation rates), prices have gone up 21% from 2005 to 2015: $100 in 2005 is worth $121.36 in 2015. So all of the suppliers to the MLS, whether that’s the staff who have to get paid or the power company with the electric bill, have raised their prices…

The consequence of not being able to raise prices is simple. The MLS has to make money somehow, and cut costs somewhere. If all suppliers and increasing their costs to you, but you can’t increase your price to your customers, you have to generate what’s called “non-dues revenues” and cut costs as much as you can.

The attempts by the MLS to generate non-dues revenues result in so many of the projects and initiatives that have brokers pissed off. Things like offering a public-facing website, charging brokers for IDX feeds, transaction management systems, broker and agent websites, market statistics, Cloud CMA, etc. etc. at steep discounts by leveraging the number of agents in the MLS — all of these things are seen by brokers (particularly larger brokers) as an unfair leveling of the playing field. Because it is. But from the MLS’s perspective, if you’re not allowed to raise prices, but your costs keep going up, you don’t have much of a choice but to try to do things to make money somewhere, somehow, no?

In terms of cutting costs, the biggest expense of the MLS is its core technology platform. A few use home-built systems, but most MLSs buy a system from MLS vendors like CoreLogic, Black Knight, FBS, and others. In that purchase process — and in the renewal process — the MLS is forced to drive costs down as low as possible because it cannot raise prices. The vendors, in turn, have to find places where they can cut costs so they make a small profit (or reduce the loss, in the case of loss-leader plays like CoreLogic’s, which offers the MLS platform at a loss to sell public data into the MLS) on the deal.

The two areas that get cut the most? Innovation and customer service.

This is a screenshot of CoreLogic’s Matrix, widely considered the best MLS platform available today. The people over at CoreLogic try their very best at producing excellent software, and do a great job with the resources they’re given…. But honestly, look at that user interface. It looks like something designed by engineers who love UNIX for the power of the command-line interface. It probably would have been embarrassing in the 90’s; it’s a disgrace in 2016.

But what choice do they have? The profit margins on MLS software are thin at best, and non-existent often. Good UI/UX (user experience) designers are expensive; in fact, they are among the most expensive talent you can hire. Something has to be sacrificed with the thin margins involved.

Same with technical and customer service. Many an MLS member (even Directors on the Board) complains that vendor XYZ is not responsive to change requests. “We put that request in nine months ago, and they still haven’t gotten to it!” At one level, it is intolerable that it takes so long to make simple changes.

But what do you expect when you’ve nickeled-and-dimed the vendors to margins that cannot support hiring more developers to work through the queue of changes that have to be made? If the margins on the product can only support three people to do bug fixes, changes, and test them… well, there are only three people who can do that, and there are only 24 hours in a day.

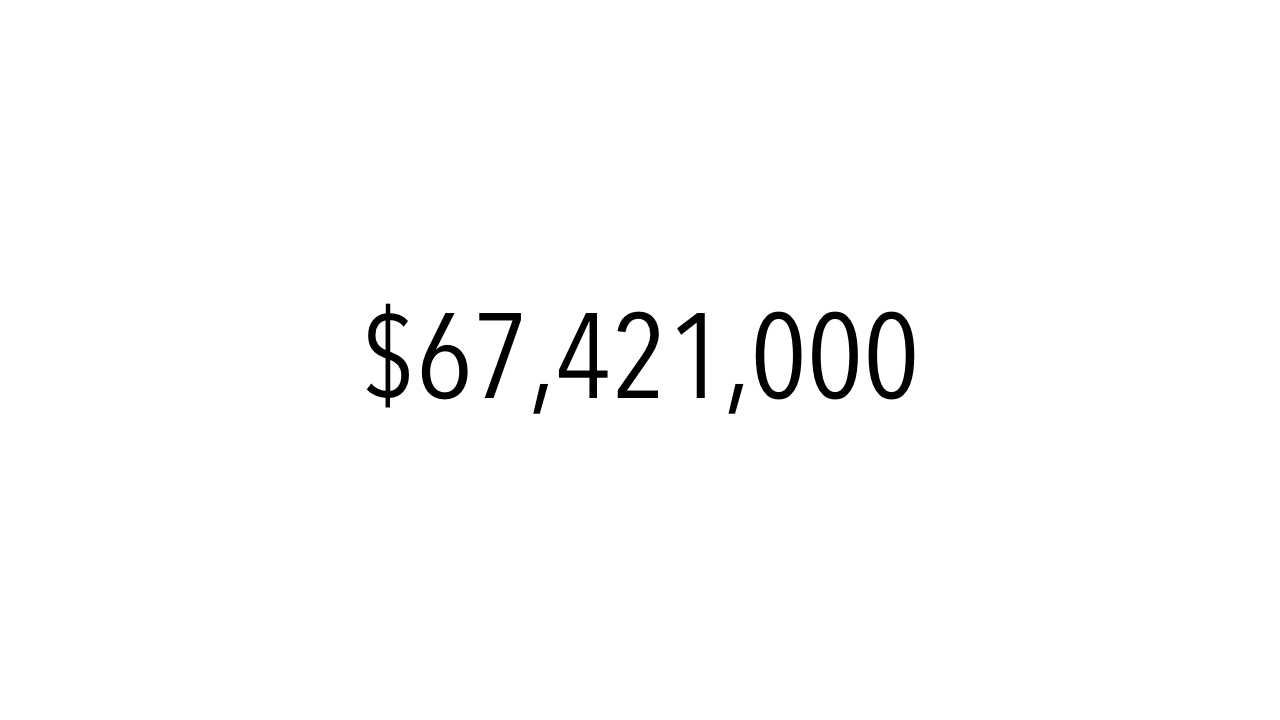

To put things in perspective, take a look at this slide from my CMLS presentation:

Do you have any idea what that number is? I’ll wait while you think about it.

.

.

[whistles Jeopardy! tune].

.

That number is what Zillow spent on Technology & Development in Q2 of 2016. One quarter — that’s three months. Annualized, Zillow will spend more than a quarter of a billion dollars just on technology and development. Let that sink in. Take a moment.

Is it any wonder that Zillow’s websites, mobile apps, and software products kick the living crap out of anything in the MLS industry? Money doesn’t mean everything in technology (or else, startups wouldn’t ever grow) but it doesn’t mean nothing. At some point, the dollars and resources available counts, and shows up in products and services.

There is not a single MLS in the country whose entire budget, never mind just the technology budget, for the entire year is $67 million. Not one.

Too many, too small, too poor — the end result is that we have 750 MLSs in the U.S. offering barely adequate (and oftentimes wholly inadequate) products and services to its customers, while branching out into all sorts of areas that its own brokers think is bullshit for the MLS to get into because of “non-dues revenues” while members complain about the cost.

I honestly don’t believe that MLS subscribers are actually complaining about the cost of the MLS; as the CRMLS example shows above, we’re talking about $35 a month or so — less than a tank of gas in most parts of the United States, and definitely less than having a cup of Starbucks latte every day. What they’re complaining about is value: what they actually get for the money.

That set of problems stems from the MLS not being able to control its own destiny as a business entity, setting its own prices and competing for business, because the governance of the MLS is seriously broken.

The Governance is Broken

That the governance of the MLS is broken might come as a shock to a few, but probably won’t be surprising to most people who read Notorious.

Sloooooow Decision Making

First sign that governance is broken is that nothing — and I mean nothing — moves fast in the MLS world. I told a story at CMLS about a developer I know who wanted to get a IDX/RETS feed from the MLS; it took four months, because the Board of Directors have to approve each and every one of those requests, and the Board had already met that month, and had decided to cancel the next month’s meeting, so wouldn’t meet until three months later. That is sadly not unusual in the MLS world.

As a consultant, I’ve done assignments for brokers, tech companies, Associations and MLSs. With brokers and tech companies, I meet with the executive (usually the CEO), have a meeting, he or she likes the proposal, and the next week, I’m working on the assignment. With Associations and MLS… I meet with the CEO, he or she likes it, and then it might be six months before we actually get started, since that has to get cleared through Executive Committee, who might send it for more study to some other committee, who will come back with recommendations, who the Executive Committee might tweak, then send to the full Board of Directors, who might make more tweaks and have more questions, and then send back to Executive Committee, who then sends it to the CEO for more clarifications….

If you got as tired of reading that convoluted sentence as I got writing it… imagine living through it. Yet, that’s the daily reality of the MLS world.

Quality of Directors

The second sign that governance is broken is in the actual individuals who serve on the Board as Directors of the company. For many an MLS, there are no real qualifications for who can be a Director, as those are positions appointed by the Association (or Associations, if a regional MLS). Sure, you might have the MLS Director position be an elected one, so the membership votes on who it should be, but as is normal in most Association politics, they’re not exactly hotly contested elections.

As a result, you often get directors of a MLS who know nothing about technology, nothing about data, nothing about corporate finance, nothing about… well… anything other than how to sell real estate. Yet, they have to make decisions that affect hundreds of even thousands of professionals who rely on the MLS to provide the technology and data backbone to their businesses.

I personally have had conversations in which it became obvious that MLS directors didn’t know the difference between a database and the data that it holds. (“Well, one is like a bottle, and the other is like the water that it holds….”) Directors didn’t know how to read income statements or balance sheets. They didn’t know the difference between debt and equity, never mind concepts like convertible bonds or multiple classes of stock. They didn’t know very basic legal concepts, like fiduciary responsibility to the corporation, or apparent authority.

In contrast, look at what a well-run company might look for in putting a Board together:

And finally, very very few (in fact, I only know of one) MLS Boards include outside independent directors. These are individuals who have no direct connection to the company or the business of that company who are brought in to offer neutral, unbiased advice to the Board as to what the company should be doing. They might be CEO’s of other companies, or political leaders, or bank presidents, or technology leaders who can offer insight to a company’s Board as disinterested experts.

Politicians make political decisions. Businesspeople make business decisions. If your MLS is governed by a bunch of politicians, it will make decisions based on politics, rather than on business realities.

That would be fine if the MLS were a political entity, whose core purpose is something like lobbying and advocacy, or upholding a standard of professionalism — you know, like the Association of REALTORS? But the MLS is a data-and-technology company that creates a marketplace for businesses that need it to conduct a real estate transaction. It is a business far more than it is a political organization.

Yet it’s governed by politicians. No wonder the MLS is so dysfunctional.

Finally, and Most Importantly, Board Representation

The main reason why the MLS governance is so messed up is that people see the Board as an extension of the Association, which is a political animal. So the most important concept in MLS Boards is representation. Big brokers want to make sure they’re “represented” on the Board, and so do small brokers. Commercial practitioners want to make sure their “voice is heard” on the Board. In a regional MLS, every single shareholder Association fights for every Board seat, because it’s about representation and having the votes, and so on and so forth.

The idea appears to be that the MLS Board is like a legislature, and the more seats you have, more control you have. And nobody wants to give up control, like ever, when it comes to the MLS. Many a MLS consolidation effort falls apart because the two Associations involved fight over how many Board seats will or will not be allocated to each one.

Thing is, all this jockeying for Board seats is utterly, completely, hopelessly pointless. And one wonders why no one has ever pointed this out.

Each individual Director, under the laws of all 50 states, and general common law principles of corporate law, is a fiduciary of the corporation of which he or she is a director. In every MLS board meeting I have ever attended, the legal counsel or the CEO starts off the meeting by reminding everyone present that they owe a fiduciary duty to the MLS itself, and instructs them to “take off your other hats”. As a fiduciary, you are supposed to consider all decisions and make your decision based on what is in the best interest of the MLS itself as an entity, not what is in the best interest of your “constituents” who have appointed you/elected you to serve on that Board.

In other words, as a Director, you are legally prohibited from representing your Association, Brokerage, Interest Group, or anybody else. Violating that fiduciary responsibility means personal liability and the corporation itself — or any of its shareholders — can sue you personally to recover damages from your bad, conflicted decisions.

So think about this. We have a situation with the MLS in which every Board member was put there by somebody to “represent them” and to “make their voices heard.” Yet, if that Board member does anything of the sort, he or she is personally liable to the MLS and to any and all of its shareholders for breach of fiduciary responsibility. A Director cannot “represent” anyone other than all of the Shareholders who collectively are the owners of the corporate entity.

Oh, by the way, corporate D&O (Directors and Officer) liability insurance does not cover breach of fiduciary duty claims, because under the law, that is a personal injury inflicted on the corporation itself by the breaching director.

All of the Associations appointing “their representative” to the Board, all of the brokers who are voting for Mr. So-and-So to represent their interests on the MLS Board — all of them are voting for nothing, since the minute that “representative director” steps into the Boardroom, he has to stop representing them and start representing the MLS corporation.

This… is literally the most illogical thing about the MLS where the poor governance structure doesn’t even do what it’s goal is to do: represent the voice of the members and the shareholder Associations.

Okay, so that’s all horrible news… how do we fix this?

How To Fix the MLS

The problem with the MLS is a structural defect that arises from the origin of the MLS as a member service provided by the local Association of REALTORS. The solution then must involve a restructuring of the MLS.

The first step is divorce from the Association. I discussed this briefly in my first post and the negative consequences of the dysfunctional marriage between the two. We’ll get into the specifics here.

The second step, that happens simultaneously with the divorce, is a restructuring of the governance of the MLS so as to make it competitive in the 21st century. Two key parts of this are: (1) keeping ultimate control over the MLS in the hands of the industry, and (2) balancing the need for proper corporate governance with the need for representation on the part of the customers.

The third step, which comes after the restructuring, is to rethink the role of the MLS and its relationship with the Participant brokers who are, after all, both its customers and suppliers of its most important asset: listing data.

The Economics of Divorce

Popular culture likes to portray marriage as the culmination of love. Truth is, marriage is fundamentally an economic union, which is why divorce is fundamentally about money: division of liability, assets, and providing for alimony and child support.

Similarly then, the divorce between the MLS and the Association is fundamentally an economic problem.

This is not the proper place to get into spreadsheets and such, so let me just post the two slides I shared with the CMLS audience and discuss them briefly. If you want a more in-depth explanation, let me know and I’ll see what I can do.

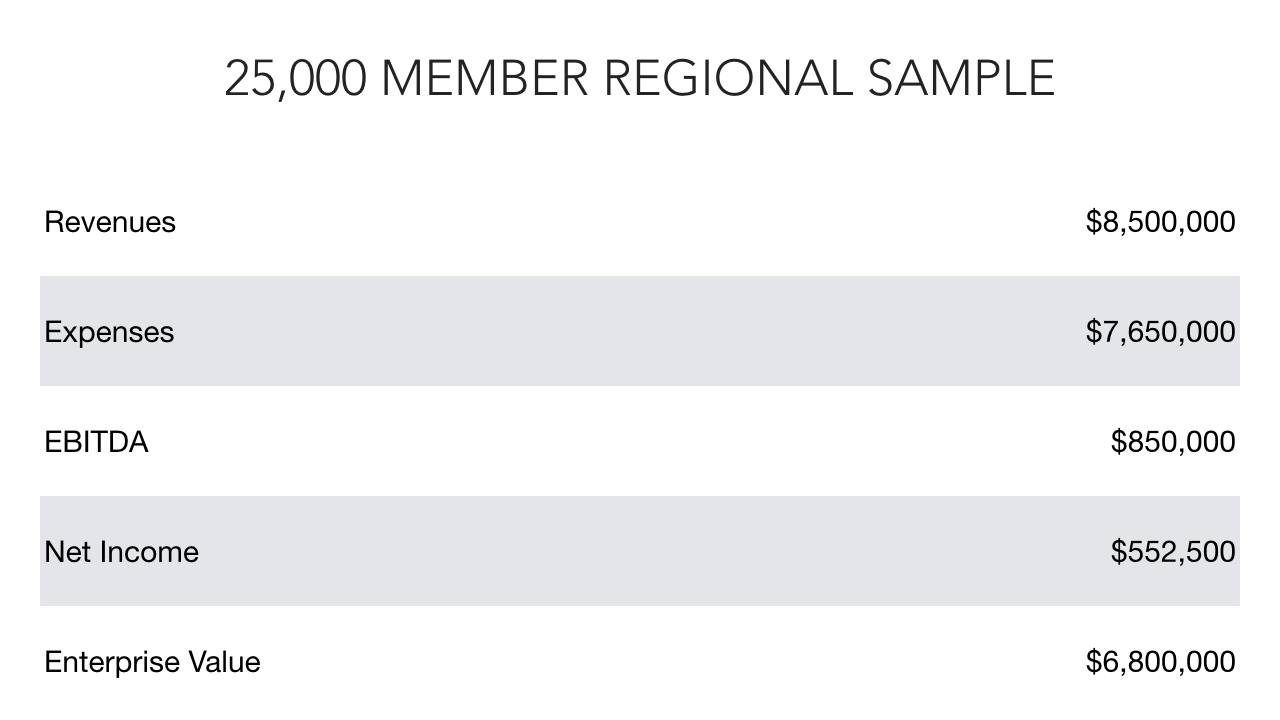

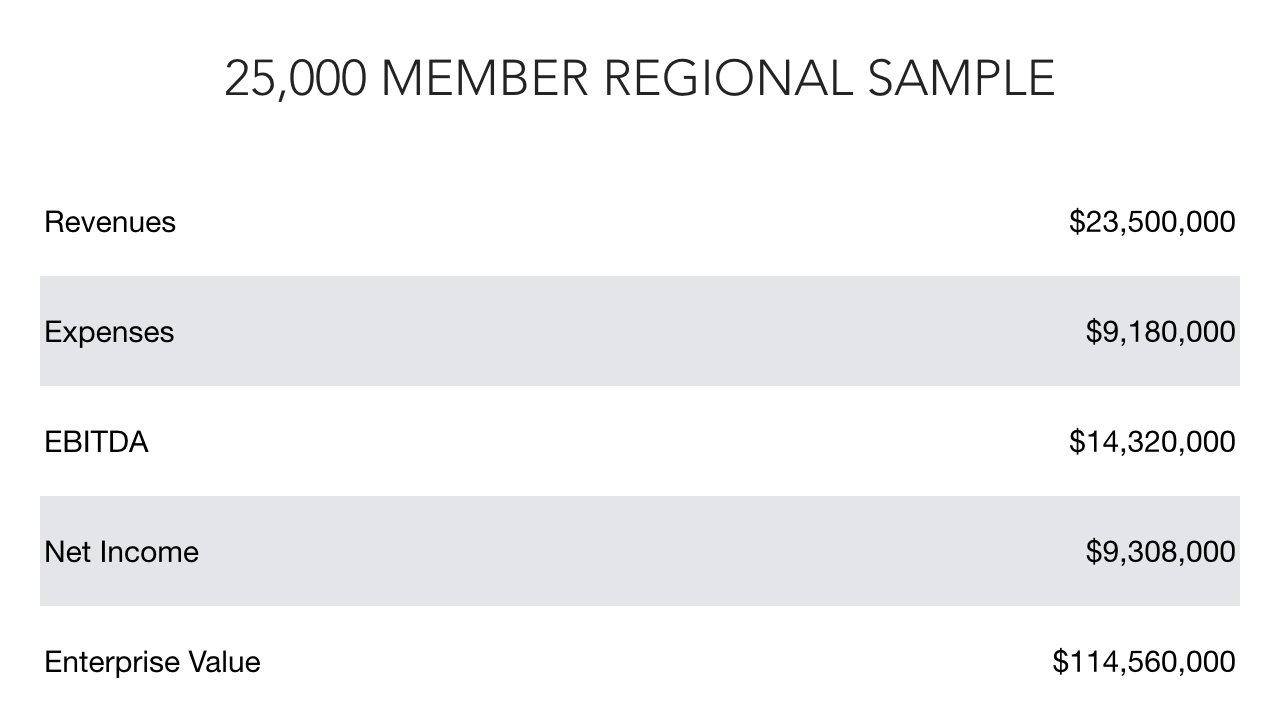

This is the MLS as is today, controlled by its shareholder Associations, and without any control over pricing. It is essentially offered as a “member service” by the Associations, and the prime directive is to operate as a non-profit. These numbers are fictional, of course, but they are drawn from real life MLSs I have worked with, and have been vetted by MLS CFO’s as being a pretty good representation of an MLS’s financials.

A couple of things to note here is that the “Net Income” is often just poured into reserves, and the “Enterprise Value” doesn’t actually mean anything. The shareholders technically own “shares” of the MLS, but those shares are economic nullities — they pay no dividends, carry no voting power (that’s setup differently in the bylaws to ensure “representation” by the shareholder Associations), and cannot be sold/traded.

In effect, the only real impact of having those shares is to have the ability to appoint directors to the Board of the MLS.

This is that same MLS post-privatization, once it is operated like a real business. Even the blind can see the dramatic increases in revenues, EBITDA, Net Income, and Enterprise Value.

I won’t beat around the bush. The biggest change here is that the price of the MLS goes from $25 a month to $75 a month — that’s right, the price triples. How in the hell do I justify that?

Pricing the MLS

If the MLS is not a “member service” (more on this later), then it has to be priced at what the market will bear. How do we even know? My reasoning was to price the MLS at the relative value it has for the customers.

I have asked numerous brokers and agents about the most important technology tools they use in their businesses day in and day out. There are variations, of course, but for the most part, the list looks like this:

Mobile phone (and tablet)

MLS

IDX website

Portals

CRM

The MLS comes in as the second most important tool in a broker/agent’s toolbox, after the mobile phone.

Well, a typical mobile phone contract for a real estate agent is about $200 a month. (This is a very rough estimate, since many providers have different pricing, and some agents have family plans with multiple lines, etc. etc.) A typical IDX website costs about $50 a month on the low-end, including the cost of the IDX property search. Portals can cost whatever the agent is buying — there are some agents who are spending $15,000 a month on portal advertising but they are, admittedly, outliers. And CRM packages can range from $40 a month to thousands of dollars a month.

My reasoning is that the MLS’s value to the customer is somewhere between the value of a mobile phone and the value of an IDX website. $75 a month seems to me to be on the low-end of that value range if an IDX website is $50 and Verizon Wireless is $200 a month.

Maybe my logic is flawed, but the only way to find out is to allow the MLS’s price to “float” against the market. What we do know today is that the price of the MLS is artificially constrained by the Board/Associations who consider it as a “member service”.

Impact on the Association

The biggest ah-ha is the impact of that cash flow on the Associations which own the MLS.

There is no reason to believe that the expenses of operating a MLS would triple if revenues triple. They would go up, but not as much as allowing free market forces into pricing does. Accordingly, the Net Income number goes from about $500K a year to over $9.3 million per year.

That corporation does and will pay regular dividends to its shareholder Associations. In every model I have built, whether using real numbers from real MLSs, or using fictional “sample” numbers, what I find is that the shareholder Associations make more money from dividends from the MLS than they would from dues income from members. That remains true even if we assume that the Association would lose 60% of its current membership overnight.

As a related aside, quite a few MLSs and Associations are structured in bizarre ways because of concerns around tax implications for the Association for generating so much income from the MLS. This is the so-called “UBIT” problem. In brief, a non-profit (like an Association) cannot generate so much income from an “unrelated business activity” without putting its non-profit status at risk. However, IRS rulings make it clear that dividends, royalties, and interest are wholly exempt from treatment as unrelated business income. The MLS will pay normal corporate income tax on its revenues, but the dividends it sends to the shareholder Associations are tax-free and do not threaten non-profit status in any way, shape, or form. That makes me think that many an MLS/Association got some really bad legal advice from its lawyers when they setup the MLS in the first place.

Post-divorce, the Association ends up with more money in its coffers than it had while it controlled the MLS and was selling it as a retail storefront. It does so with fewer members.

Furthermore, the Enterprise Value becomes meaningful. Those shares are no longer economically meaningless, because they can be bought, sold, and traded, and since the MLS pays dividends, those shares have prices that can be calculated.

In the example used above, I have posited four shareholder Associations, with different numbers of subscribers and different numbers of shares. The largest, with 10,000 of the 25,000 subscribers, ends up with shares worth $45.8 million — half of which can be freely traded — while the smallest, with 3,000 of the 25,000 members, ends up with shares worth $13.7 million — again, half of which can be freely traded.

If you can identify another way for a REALTOR Association to generate $45.8 million in wealth (i.e., assets), I’d like to hear about it.

With its finances secure without having to worry about membership dues, the REALTOR Association can become what it needs to become: an exclusive group of real estate professionals who uphold the ideals of the Preamble — Advocacy to protect homeownership, and Professionalism that goes beyond ordinary commerce. That’s the whole reason for all of this work, after all.

Restructuring the Governance

Simultaneously with the Divorce, the governance of the MLS is restructured. There are three goals here:

Allow the MLS to operate like a real business

Never lose ultimate control over the MLS

Create representation so that the broker/agent voice can be heard

The way we accomplish all three is as follows. We start with #2, as it leads to the other two.

We create two classes of shares for the MLS. Class A shares are voting shares, and come with a variety of restrictions as to who can own them, how, and under what terms. Class B shares are investor shares, which have no (or reduced) voting power, but comes with no restrictions on ownership.

As long as the current shareholders — all Associations for the vast majority of MLSs in the country — hold on to Class A voting shares, there is no possibility that any third party outside entity can “take over” the MLS.

The Board of Directors, then, are elected by all of the Class A shareholders voting their shares, as in any normal corporation. They represent nobody, except all of the shareholders as a collective. Like any corporate Board, the MLS Board concerns itself with financial and business matters. Its essential job is to hire the right CEO to run the company, and to hold the CEO accountable.

“But that means the REALTOR loses his voice on the most important tool he has!” might be the objection. Not true. (First, REALTOR has no control over Samsung, Apple, Verizon or AT&T who control her most important tool… but I digress.)

Instead of putting the burden of representation on the Board, which is self-defeating for reasons laid out above, we create a new body. We’ll call it the “Stakeholder Advisory Council” or SAC for now. This body can be fully representative in any way that the MLS and its stakeholders want. You want Large/Mid-size/Small Broker seats on the SAC? No problemo. Each shareholder Association should have seats? No problem. Want women represented? No problem. Commercial? Okee-dokee.

This group has no legal authority to bind the Board, the CEO, or the corporation in any way. That’s important to avoid being classified as a fiduciary under corporate law. But in practical terms, the SAC is enormously powerful because many of those seats are appointed by organizations that have Class A voting shares, and those shareholders elect (and dismiss) the Board of Directors.

Imagine if the Board consistently ignores the recommendations of the SAC, and runs roughshod over SAC resolutions. Every member of SAC represents (and I mean truly represents, since they’re not bound by any other duties to the MLS or otherwise) constituents who are important stakeholders in the MLS. Many are direct representatives of the shareholder Associations. How quickly will that recalcitrant Board of Directors last in that situation?

Rethinking the MLS: Participant Brokers

It’s just a marketplace after all…

The final piece of the puzzle, which can happen either simultaneously or after the above two structural changes happen, is to rethink the relationship between the MLS and the Participant Brokers who may or may not be members of the local Association.

Every financial model I have built shows enough in Net Income to provide for a Broker Profit Share, and I strongly recommend that privatization incorporate that element.

The concept is pretty simple. The MLS is transformed into a money-making commercial venture. It is able to have that venture only because its Participant brokers put listings into the MLS. For all the talk about companies making money off the backs of brokers, the MLS is at the forefront of those companies.

Accordingly, the MLS should share back some of the profits it has earned with those Participants who are providing it with the assets it uses to generate that profit in the first place.

In the 25,000 person sample provided above, I have modeled out 15% profit share, which amounts to about $1.4 million in annual profits given back to its Participant brokerages on a pro-rata basis, based on the number of listings put into the MLS. That is entirely passive income for those brokerages, and a concrete example of monetizing the value of their listings.

Furthermore, once the artificial cap on pricing is lifted, the intelligent MLS CEO and Board would rightly ask whether they still need to engage in all these “non-dues revenues” programs that aren’t generating a whole lot of income, but generating a whole lot of resentment.

In this context, it is worth asking what the value of a well-organized marketplace with rules and regulations that are consistently enforced is. What is the value of a marketplace where buyers and sellers know what the expect from the other side?

NASDAQ, as an example, charges $1,000 per month per person as a subscription fee. And NASDAQ doesn’t even provide any software or a front-end for that: merely the right to access the NASDAQ marketplace. That’s how valuable a well-ordered, well-organized marketplace is to practitioners.

Products and Services Improvements

It should be obvious, but just in case….

One of the outcomes of privatization is that the MLS has money and resources it has never been allowed to have before. As I described above, the MLS offers products and services that are crap because it doesn’t have the money to invest into products and services that aren’t crap. Well, that changes, doesn’t it?

CRMLS, which I used as an example above, with 82,000 subscribers would generate (under the assumptions above) revenues of $75 million, post-tax profits of $43 million, and have Enterprise Value in excess of half-a-billion dollars. It is now a Mid-Sized business, according to Gartner, and can invest tens of millions of dollars into dramatic improvements in MLS platform technology, data, and customer service.

Upstream with its less-than-$12 million in funding no longer seems like a scary competitor, but an impoverished startup trying to take on the MLS that is throwing off four times that amount in Net Income. And oh by the way, everything that the Brokers want from Upstream can be provided by the MLS in no-time-flat given the additional resources provided to the MLS world.

That’s the future of the MLS. And it’s not a pipe-dream but a hard cold numbers-and-facts reality, if the industry would only reach for it.

Wrapping Up

I know this got long, but it was an important chapter to lay out.

The problems of the MLS are not insurmountable. They can be addressed, and the structural defects of the MLS can be fixed. The result of those fixes is more money than ever imagined possible to the MLS and to the Associations that own them, which liberates both from artificial political constraints of today, so that both can live up to what they can and should be.

In future parts of this series, I’ll address the further consequences of privatization on both the Association and the MLS, specifically consolidation. What does MLS consolidation look like if we take politics out of it, and put business in it?

I realize that as long and semi-detailed as this is, your local situation may be different, and you may have a bunch of questions. Feel free to contact me for more detail, as a blog isn’t necessarily the best medium to have that dialogue.

Comments and questions are, of course, welcome as always.

Managing Partner of 7DS Associates, and the grand poobah of this here blog. Once called "a revolutionary in a really nice suit", people often wonder what I do for a living because I have the temerity to not talk about my clients and my work for clients. Suffice to say that I do strategy work for some of the largest organizations and companies in real estate, as well as some of the smallest startups and agent teams, but usually only on projects that interest me with big implications for reforming this wonderful, crazy, lovable yet frustrating real estate industry of ours.

Get NotoriousROB in your Inbox

8 thoughts on “Heaven’s Got A Plan For You: The MLS – Future of Organized Real Estate, Part 2”

Technologist’s takeaway from Rob’s post:

“But what do you expect when you’ve nickeled-and-dimed the vendors to margins that cannot support hiring more developers to work through the queue of changes that have to be made? If the margins on the product can only support three people to do bug fixes, changes, and test them… well, there are only three people who can do that, and there are only 24 hours in a day.”

Technologist’s comment on the takeaway:

Three people … if you’re lucky. 2 expert/competent people if you’re “very” lucky.

You guys haven’t figured out yet , we Agents need to do a Reexit like the brave British people did, get rid of the lousy mls,s and the shakedown artists at nar, abolish the pacs used to collect bribes for Congress and the state houses,this will go a long way to cleaning up the RE business.

Great article and accounting Rob. Spot on. I heard a rumor that 135 MLSs read this and are considering what you have proposed – that they fully restructure the MLS; get a divorce from the Associations and triple the member dues now. They indicated that they would get back to you with thoughts and suggestions in six to ten months after they conducted a poll of their collective 350,000 members for an opinion on all this and then consider the degree of change they think is needed now as 135 independent Committees. One MLS executive told me to covey to you to – “hey, great idea, just hold onto that thought.”

Hi Rob

No question there is loads more grey hair. It’s the less visible signs that worry me more!

The challenge for most MLS’ is that of all the critical stakeholders (brokers, agents, associations, staff, partner/vendors and of course consumers) one or more of these important constituents invariably get relegated to the kid’s table at Thanksgiving dinner. And as invariably happens, when one of us gets abit unruly, we get sent to our room.

In the mid-Atlantic, we are attempting to bring everyone into the tent as we believe all are critical to the success of this initiative and by association, the industry. This process is more complex but also eminently doable. It takes time; lots of it. It takes enlightened thinking which requires suspending judgement. It takes money as there is no better way to ensure cooperation. Importantly it takes the willingness to listen.

This is the recipe for MRIS and TREND and the very enlightened, contiguous markets that are on this journey. Those of us charged with creating the future cannot be wedded to the status quo. Stay tuned!

Hi David – As I was reading this I was wondering if MLS Evolved is open to non-Realtors, and if so how are the Associations handling it?

Are you kidding, is that a serious question?,none of the lousy mls’s will allow that,big daddy aka nar would slap them around,great question,any bets on a response.

Tego, much to the chagrin of one of the respondents to this blog, individuals licensed by the state but not belonging to a Realtor association can belong to MLS:Evolved (new name on the horizon) just as they have been able to do with MRIS since inception.

Enlightening article, let the trumpet sound! Something needs to happen.

Each individual Director, under the laws of all 50 states, and general common law principles of corporate law, is a fiduciary of the corporation of which he or she is a director. In every MLS board meeting I have ever attended, the legal counsel or the CEO starts off the meeting by reminding everyone present that they owe a fiduciary duty to the MLS itself, and instructs them to “take off your other hats”. As a fiduciary, you are supposed to consider all decisions and make your decision based on what is in the best interest of the MLS itself as an entity, not what is in the best interest of your “constituents” who have appointed you/elected you to serve on that Board.

Each individual Director, under the laws of all 50 states, and general common law principles of corporate law, is a fiduciary of the corporation of which he or she is a director. In every MLS board meeting I have ever attended, the legal counsel or the CEO starts off the meeting by reminding everyone present that they owe a fiduciary duty to the MLS itself, and instructs them to “take off your other hats”. As a fiduciary, you are supposed to consider all decisions and make your decision based on what is in the best interest of the MLS itself as an entity, not what is in the best interest of your “constituents” who have appointed you/elected you to serve on that Board.

Furthermore, the Enterprise Value becomes meaningful. Those shares are no longer economically meaningless, because they can be bought, sold, and traded, and since the MLS pays dividends, those shares have prices that can be calculated.

Furthermore, the Enterprise Value becomes meaningful. Those shares are no longer economically meaningless, because they can be bought, sold, and traded, and since the MLS pays dividends, those shares have prices that can be calculated.

8 thoughts on “Heaven’s Got A Plan For You: The MLS – Future of Organized Real Estate, Part 2”

Technologist’s takeaway from Rob’s post:

“But what do you expect when you’ve nickeled-and-dimed the vendors to margins that cannot support hiring more developers to work through the queue of changes that have to be made? If the margins on the product can only support three people to do bug fixes, changes, and test them… well, there are only three people who can do that, and there are only 24 hours in a day.”

Technologist’s comment on the takeaway:

Three people … if you’re lucky. 2 expert/competent people if you’re “very” lucky.

You guys haven’t figured out yet , we Agents need to do a Reexit like the brave British people did, get rid of the lousy mls,s and the shakedown artists at nar, abolish the pacs used to collect bribes for Congress and the state houses,this will go a long way to cleaning up the RE business.

Great article and accounting Rob. Spot on. I heard a rumor that 135 MLSs read this and are considering what you have proposed – that they fully restructure the MLS; get a divorce from the Associations and triple the member dues now. They indicated that they would get back to you with thoughts and suggestions in six to ten months after they conducted a poll of their collective 350,000 members for an opinion on all this and then consider the degree of change they think is needed now as 135 independent Committees. One MLS executive told me to covey to you to – “hey, great idea, just hold onto that thought.”

Hi Rob

No question there is loads more grey hair. It’s the less visible signs that worry me more!

The challenge for most MLS’ is that of all the critical stakeholders (brokers, agents, associations, staff, partner/vendors and of course consumers) one or more of these important constituents invariably get relegated to the kid’s table at Thanksgiving dinner. And as invariably happens, when one of us gets abit unruly, we get sent to our room.

In the mid-Atlantic, we are attempting to bring everyone into the tent as we believe all are critical to the success of this initiative and by association, the industry. This process is more complex but also eminently doable. It takes time; lots of it. It takes enlightened thinking which requires suspending judgement. It takes money as there is no better way to ensure cooperation. Importantly it takes the willingness to listen.

This is the recipe for MRIS and TREND and the very enlightened, contiguous markets that are on this journey. Those of us charged with creating the future cannot be wedded to the status quo. Stay tuned!

Hi David – As I was reading this I was wondering if MLS Evolved is open to non-Realtors, and if so how are the Associations handling it?

Are you kidding, is that a serious question?,none of the lousy mls’s will allow that,big daddy aka nar would slap them around,great question,any bets on a response.

Tego, much to the chagrin of one of the respondents to this blog, individuals licensed by the state but not belonging to a Realtor association can belong to MLS:Evolved (new name on the horizon) just as they have been able to do with MRIS since inception.

Enlightening article, let the trumpet sound! Something needs to happen.

Comments are closed.